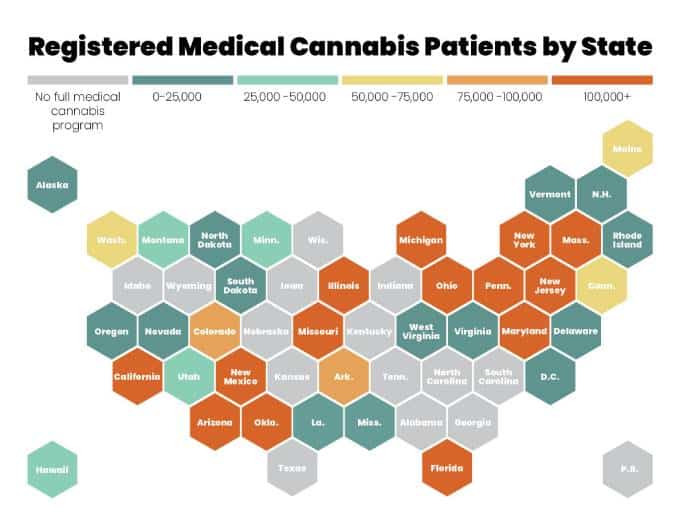

An overview of state medical cannabis markets by patient count, with commentary from Headset.

As more states allow for adult consumption of cannabis, it’s important to look at how full legalization is affecting medical cannabis markets. Currently, there are 39 states that have legalized medical cannabis, and 19 states that have legalized adult use. Besides South Dakota, every state that has legalized adult use had already legalized medical cannabis at an earlier date.

While the path to legalization—prohibition to medical to recreational—is standard, there are some significant differences and similarities between states that have transitioned from medical to adult use that are worth examining. In particular, we analyzed medical and adult-use sales numbers and looked at average basket size and category preferences in both medical and adult-use markets.

Early on, states were slow to transition from medical to adult legalization. California, which in 1996 was the first state to approve medical use, didn’t approve adult use until 20 years later, in 2016. This transition has moved a lot faster in recent years, in states like Illinois, which passed medical in 2013 and adult use in 2020. Generally speaking, states with relatively mature recreational markets share some distinctions that differ from newer recreational markets.

But there are a lot of other factors at play that affect adult-use and medical markets.

Sales in States That Recently Opened Recreational Markets

To begin, we’ll look at Illinois and Michigan markets, as they have both made the transition from medical only to medical and adult use within the last two years. When adult-use markets open, they tend to grow at a rapid pace. Sales in Illinois, for example, grew by 226% from $39.2 million, when they first began in January 2020, to $127.8 million in July 2021. Over this same time period, Michigan’s total adult-use sales grew from only $9.8 million to $115.3 million, a whopping 1,077%.

As adult-use sales skyrocketed in both states, medical sales in Illinois have meanwhile remained fairly consistent, with a total increase of 35% from $23.4 million in January 2020 to $31.5 million in July 2021. Medical sales in Michigan grew by 75% over this time period—what would be considered a respectable, high growth rate in most industries, but a number that pales in comparison to the state’s colossal growth in adult-use sales.

It is clear that the introduction of adult-use sales leads to a decrease in medical sales proportionally. In July 2021, medical sales in Illinois reached an all-time low, accounting for only 20.9% of all sales (down from a high of 45.5%). Michigan medical sales have also steadily declined proportionally, accounting for only 27.7% of all sales in the state by July 2021 (down from a high of 73%). That being said, it’s certainly not the case that adult-use markets are making their medical counterparts irrelevant—remember in both of these markets, adult-use sales still grew respectively.

Perhaps adult-use markets help legitimize cannabis and signal to more people with medical ailments that cannabis can help their condition.

Sales in States with More Mature Recreational Markets

When looking at states that have recently entered the recreational space, we see a steady decline in proportional medical sales relative to adult-use sales. In more mature markets, however, the proportions of medical to adult-use sales stay pretty flat. For example, in Colorado, which introduced adult-use cannabis back in 2014, medical sales have accounted for 18 to 23% of total cannabis sales from January 2020 to July 2021. And in Oregon, which introduced adult use in 2015, medical sales have hovered between 8 and 12%.

Why Do Patients Still Use Medical Programs?

When looking at sales data, it’s clear that even though recreational sales trump medical sales, state medical programs are still alive and well. Besides the legitimacy factor—cannabis has medicinal properties that can help people in need—there are several other reasons why people would opt for medical over adult use and pay the expenditure for a medical card.

- ● Lower age limits: In states like Oregon and Colorado, the age limit for medical use is 18, while the age limit for adult use is 21. This may incentivize younger consumers to procure a medical card, so they can purchase from dispensaries.

- ● Lower taxes: Medical cannabis purchases, in general, are taxed at appreciably lower rates than adult use. For example, in Colorado adult-use sales are subject to a 15% cannabis excise tax and any additional local taxes, whereas medical sales are subject to only a 2.9% state excise tax plus local taxes. In Oregon, medical purchases aren’t taxed at all, whereas recreational purchases are subject to a 17% excise tax and an additional 3% local municipal tax.

- ● Higher-THC potency products: Some markets have higher product THC potency limits for medical products compared to recreational. In Washington, for example, a recreational edible is limited to 100mg THC per package and 10mg THC per serving, whereas a ‘High THC’ product available only to medical patients may contain up to 500mg THC per package and 50mg THC per serving.

- ● More knowledgeable staff: Some markets require budtenders to have more training or experience in order to sell medical cannabis, as opposed to just selling recreational. For example, Washington has a program for cannabis retail employees to become certified medical marijuana consultants, which requires 20 hours of training. Medical patients who are perhaps newer to cannabis or are really dedicated to finding the right products to treat their condition, would welcome having more knowledgeable staff to guide them.

Distinguishing Buying Patterns For Adult-Use Consumers VS. Medical Patients

In addition to sales numbers, through our research, we found other notable differences between medical and adult-use markets. Sales data suggests medical patients and adult-use customers have different general preferences across product categories, with medical patients more likely to purchase concentrates and adult-use customers more likely to purchase edibles and pre-rolls.

This makes sense, as medical patients may need a product with higher intensity to help alleviate pain, whereas edibles and pre-rolls are portable and shareable, appealing to adult-use consumers who may be using cannabis more for fun and socialization than to treat ailments. Flower and vape pens, in contrast, are popular amongst both medical patients and adult-use consumers; we didn’t find any discernible differences for these categories.

Another trend we found is in basket size. Medical patients on average purchase more goods per transaction than adult-use customers.

This makes sense because there are a lot of adult-use customers who just dabble in cannabis and perhaps want to visit dispensaries for the novelty of it, so they’re less likely to purchase a lot. Medical patients had to pay a fee to access their program and the money spent could signal they’re more committed to purchasing cannabis than adult-use consumers as a whole. A lot of medical patients find serious relief through cannabis and are therefore more likely to use cannabis consistently and purchase more products. Also, there are medical patients who have ailments that make it harder to visit dispensaries, so they’re more inclined to buy a lot of products at once, rather than making frequent trips.